The Case That China Is Now Actively Resisting Pressure on the Yuan to Appreciate

For a while now the smart take on China’s currency has been that it isn’t really an issue for the U.S. or Europe because, if anything, China has been propping its currency up.

After all, China is mired in a five-year long property market slump—and Chinese interest rates are well below U.S. rates. Xi hasn’t exactly been friendly to China’s tech tycoons, or to any entrepreneur who challenges the primacy of the party. Money is pouring out of China (at least foreign direct investment is on net pouring out of China).*

All accurate points.

But the overarching conclusion that the yuan is under pressure to depreciate against the dollar is now, in my view, out of date.

The preponderance of evidence suggests that China has been resisting pressure on its currency to appreciate (against the dollar) for most of the past year (the main exception is the month of April, when the U.S. briefly raised tariffs on China to 145 percent).

The data points here all line up, more or less—particularly if it is taken as a given that the state commercial banks now do most of the day to day management of the currency (I think folks in the market believe this, I think the U.S. Treasury suspects it is true, and I worry that the IMF hasn’t looked at it at all seriously for reasons that are above my pay grade).

Consider the following:

a) China’s state commercial banks added $47 billion to their net foreign asset position in the month of June. That brings accumulation in Q2 up to $70 billion, and follows on $95 billion in Q1, $75 billion in Q4 and $65 billion in Q3.

b) The balance of payments data, which covers the policy banks as well, tells a similar story. The yuan is now trading strong relative to the fix.

c) FX settlement, which lagged the formal balance sheet numbers, has also now turned positive. Net FX settlement for the first two months of Q2, adjusted for swap contracts, was a positive $47 billion; Q2 should show purchases of over $60 billion.

d) Bloomberg has reported that the Chinese state banks are now lending, not borrowing, dollars in the offshore FX swaps market. Back in the day when the state banks were doing a backdoor defense of the yuan, they would borrow dollars in the swaps market and then sell them spot (with the forward leg of the swap invisible to most eyes, as it is off-balance sheet and not disclosed):

“By borrowing dollars to buy yuan via swaps trades, Chinese banks essentially supported the yuan exchange rate, while foreign investors gave the Chinese banks dollars and got the equivalent in the yuan to invest in the local bond market. Chinese state-owned banks had been cutting their greenback borrowings via one-year swaps since the second quarter, according to traders. They’re now offering short-term greenback via swaps.”

e) Chinese policymakers are talking about allowing more private outflows—something that they normally do only when there are substantial inflows that they want to offset.

These data points all paint a consistent picture: one where the inflows from China’s massive trade surplus ($115 billion of goods in June, which translates to roughly $100 billion in goods and services if June services trade maps to trend) are even larger than the desire of private Chinese firms and investors to get money out of China.**

Hence the $47 billion in state bank foreign asset accumulation in June. That was only partially offset by a $10 billion fall in foreign exchange reserves—as China seems to have a conscious policy of running down its FX reserves at a very modest pace these days.

This change in the direction of pressure matters enormously for policy.

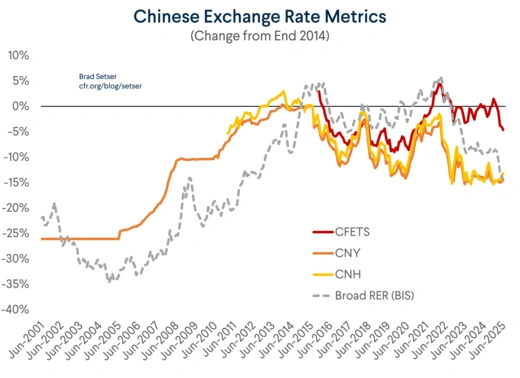

The yuan has been more or less fixed to the dollar for most of the last two years.

The de facto tight linkage to the dollar has clearly become a bit of a problem for many of China’s trading partners in 2025, as the yuan followed the dollar down. Throw in the yuan’s depreciation against the dollar in 2023 and ongoing deflation in China, and China’s real effective exchange rate is now extremely weak.

It has fallen by close to 20 percent over the last three years. That is a massive move, and one that in any conventional model would increase China’s net exports and its external surplus by about 3 percentage points of China’s GDP (or by about half a point of world GDP). I thus don’t think it is an accident then that net exports have added close to 2 percentage points of GDP to Chinese growth over the last four quarters of data.***

The U.S., which is (belatedly) adjusting the methodology of the foreign exchange report to include the activities of state banks and Asian sovereign pension and wealth funds, is likely to have real cause if they want to make currency an issue in the October foreign exchange report.****

But the truly interesting policy question is for Europeans, who historically have treated China’s currency management as someone else’s problem.

The Germans historically haven’t wanted anyone to focus on large balance of payments surpluses either. It only made life uncomfortable in Berlin.

The Commission—which represents the European Union and has no real responsibility for fiscal policy (mostly a national competence, with the commission in theory policing against large fiscal deficits) or currency policy—also doesn’t feel comfortable with currency issues, which are mostly the domain of the ECB (which only represents the euro area, not the full European Union).

But the issue is increasingly pressing for the euro area—and it is a topic where the leaders of Germany (on the front lines of the China shock, with decreasing exports as German industry loses out to China), France (with an external deficit and concerns about the French auto sector) and Italy (which still has a large manufacturing sector that is also exposed to China’s export boom) should be able to agree.

In fact, it would be a very suitable topic for the G7 collective action—and maybe something that the French G7 presidency could take on. It wouldn’t be unreasonable to ask China to allow some appreciation at a point in time when the market is already pushing in that direction.

More generally, the only real way to bring about a more balanced world economy is for the two biggest components of the global economy—China and the United States—to have more balanced domestic economies. The easiest way to bring that about would be through an appreciation of the yuan.

* The chart below broadly illustrates China’s FDI flows

** China has significant capital controls, which can and do impact the balance between private outflows and the inflows from the trade surplus.

*** In fairness, the number here may have been inflated by the use of the BOP goods data—as the BOP surplus adjustment shifted a bit, and that raised BOP exports relative to customs data. Conversely, the BOP adjustment reduced the contribution of net exports to growth in the past. But the basic story is certainly true: the underlying export volume data points to a similarly large contribution, as export volume growth over the last 12 months has easily been 10 percentage points higher than import volume growth.

**** Politics though may get in the way; Trump wants a state visit to China.